America’s Home Loans: Your Guide to Navigating America’s Mortgage Market

America’s Home Loans: Your Guide to Navigating America’s Mortgage Market

Profiting from homeownership in the United States requires more than just finding the right house—what truly empowers buyers is understanding the intricate landscape of home loans and financing options. America’s Home Loans: Your Guide to Financing breaks down the critical components of securing mortgage credit, from loan types and credit requirements to market trends and strategic advice. With rising housing costs, evolving regulatory frameworks, and shifting interest rates, today’s borrowers face a complex but increasingly accessible path to homeownership—if guided by accurate, actionable knowledge.

The Foundation of Home Loans: Common Types and How They Work

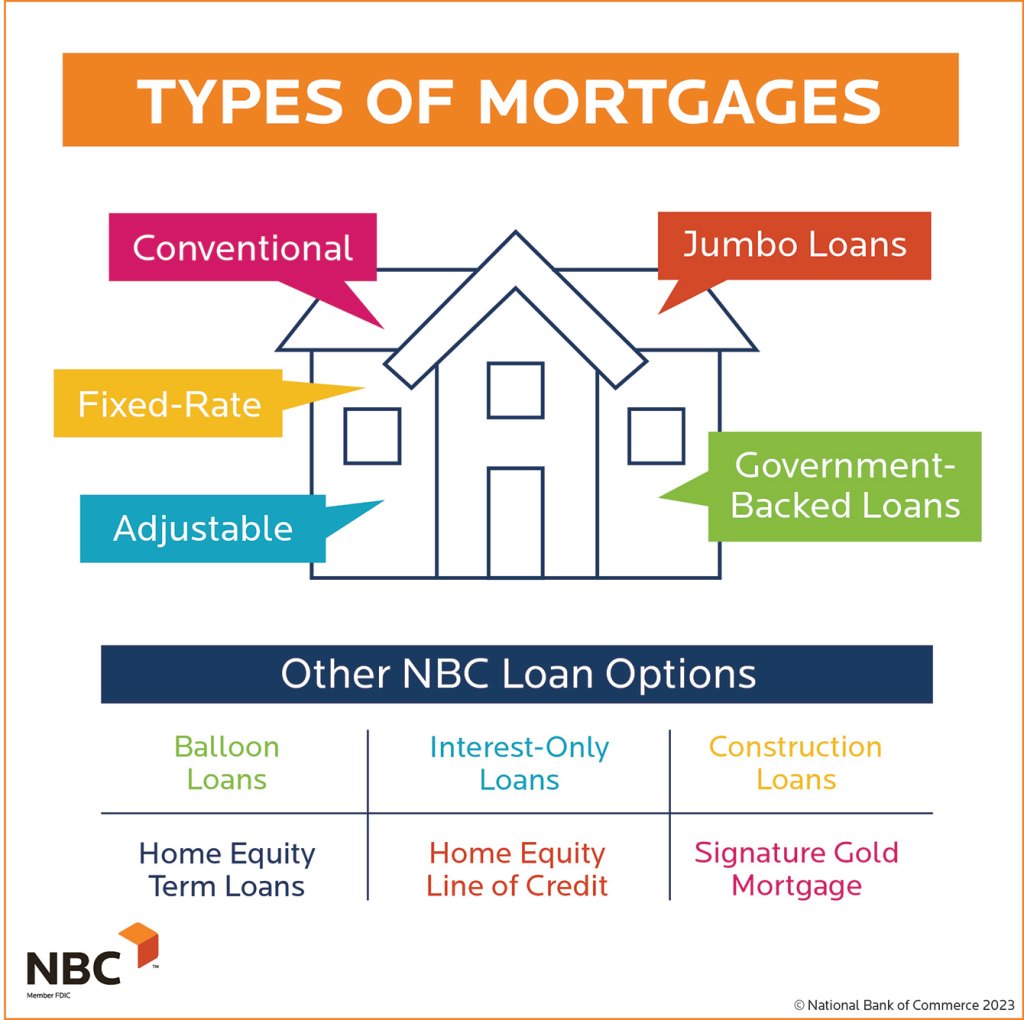

At the core of American mortgage financing are several standard loan products, each tailored to specific financial profiles and life goals. The most prevalent includeFixed-Rate Mortgages, where interest stays constant over the loan term; Adjustable-Rate Mortgages, which begin with lower rates but adjust periodically; and Government-Backed Loans such as FHA, VA, and USDA loans, designed to extend homeownership access to underserved and long-term homeowners. Fixed-rate loans offer predictability, making budgeting easier.For example, a 30-year fixed rate can mean that a $300,000 mortgage locks in the same monthly payment for three decades. In contrast, adjustable-rate mortgages (ARMs) often begin with intially competitive rates—sometimes significantly lower than fixed rates—but carry uncertainty tied to market shifts. FHA loans, backed by the Federal Housing Administration, require minimal down payments (as low as 3.5%) and relaxed credit standards, serving first-time buyers and lower-income households.

The VA loan, exclusive to military veterans and eligible service members, typically offers zero-down financing and zero private mortgage insurance (PMI), reducing both upfront and long-term costs. Meanwhile, USDA loans target rural buyers, with substantial down payment exemptions and competitive interest rates. Choosing the right loan depends on tenure plans, risk tolerance, and financial capacity—critical considerations often misunderstood by first-time buyers.

Credit Scores and Loan Eligibility: The Gatekeepers of Borrowing

Lenders evaluate three key components when assessing mortgage applications: credit history, debt-to-income ratio, and overall financial stability. At the forefront is the credit score—a critical determinant of loan terms and approval likelihood. The standard FICO ranges from 300 to 850, with scores above 620 generally needed for conventional loans, though FHA and VA loans often accept scores as low as 620 to 660.According to industry data, a FICO score of 760 qualifies borrowers for the most favorable interest rates, sometimes below 4%, while a score below 620 may trigger hybrid loan structures or require larger down payments to offset perceived risk. This underscores the importance of maintaining strong payment history and minimizing revolving debt prior to applying. Credit utilization—and the so-called “credit mix”—also influences outcomes.

Experian notes that lenders favor a balanced credit profile: responsible use of credit cards paired with managed installment loans signals long-term reliability. Debt-to-income (DTI) ratios are equally pivotal—measuring monthly debt obligations against gross income. Typical underwriting standards allow DTIs up to 43%, though prime lenders often prefer values under 40%.

Exceptions exist for self-employed borrowers or those with strong payment histories, but transparency in financial reporting remains essential.

Understanding Loan Terms, Rates, and Hidden Costs

Mortgage financing extends beyond the stated annual percentage rate (APR); borrowers must account for a range of associated fees and rate structures that dramatically affect total borrowing costs. The points system, introduced at origin, allows buyers to pay fees upfront in exchange for lower interest rates—known as “disc.stylePolicy” in some lender platforms.A “zero-point” mortgage, for instance, costs buyers a $3,000 fee in exchange for a 30-year rate 0.25% below the prevailing market rate. Interest rates themselves are influenced by national economic indicators, including Federal Reserve policy, inflation trends, and Treasury yields. Over the past three years, rising rates pushed 30-year mortgage averages above 7%, though recent slowdowns have brought rates back toward the 5–6% range.

Equally important are closing costs, which typically total 2–5% of the loan amount. These encompass fees for title insurance, appraisals, title searches, and origination charges—non-negotiable yet often misunderstood components. For example, while appraisal fees average $400–$600, title insurance—required to protect against ownership disputes—ranges from $500 to $2,000 depending on state and loan amount.

Borrowers must also distinguish between nominal and effective rates. APR reflects total annual costs including interest and fees, offering a standardized measure—critical for comparing loan offers. Ignoring these nuances can inflate long-term expenses by thousands of dollars.

Strategic Pathways: Aligning Loans with Financial Goals

Selecting the “best” home loan hinges on aligning financing with personal circumstances and forward-looking priorities. For vendors accustomed to traditional mortgage structures, exploring alternative options can unearth significant savings and flexibility. Government-backed loans, though often maligned for insurance premiums, open doors for buyers with limited savings or non-prime credit.The FHA loan’s 580–600 credit score minimum enables access where conventional loans fail, though upcoming settPurposeovation of FHA underwriting rules may tighten guidelines in 2025, particularly for high-risk markets. VA loans, exclusive to eligible service members, eliminate PMI entirely—protecting borrowers from fees that add $300 to $600 monthly in interest. Given over 23 million veterans serve in the U.S.

military, leveraging VA benefits represents hundreds of billions in long-term value. For long-term stayers, fixed-rate mortgages remove the volatility of ARMs, providing stability through market swings. Conversely, adjustable-rate products may suit consumers planning to sell or refinance within five to ten years—a window during which rate caps—often 2% annually—limit exposure.

However, flexibility demands discipline: longer loan terms stretch monthly payments but increase total interest. A 30-year vs. 15-year fixed comparison reveals stark differences—double the term may slash payments by ~$400 monthly but cost over $200,000 in extra interest.

Shorter ARM terms, though not detailed here, frequently pair well with rising rate environments, allowing early refinancing at lower rates while locking in initial affordability. Recent market trends also spotlight rising demand for “no-cost” and “low-income” mortgage programs. States like California and New York have expanded down payment assistance and credit counseling initiatives, integrating financing education with direct aid to reduce barriers.

“Home loans are not one-size-fits-all,”” says Maria Chen, a mortgage specialist at First National Realty. “The key to successful financing lies in matching loan features—rate structures, down payment needs, and term lengths—to individual financial realities and long-term visions.”

Beyond numbers, understanding the emotional and psychological weight of borrowing is vital. Citizenship, stability, and wealth-building are deeply tied to homeownership.Yet, the stress of unmanageable debt or hidden fees can erode trust in the system. Financing guidance thus must balance technical clarity with empathy—empowering buyers not just to qualify, but to thrive.

In an era of digital lending platforms and AI-driven underwriting, the fundamentals remain unchanged: know your credit, understand trade-offs, and plan beyond principal and interest.

America’s home loans, when navigated with informed intent, offer a gateway to lasting financial freedom—one calculated step at a time.

Related Post

Evan Mock’s Net Worth Revealed: From Rising Star to Celebrated Entertainer

The Unstoppable Influence of Paige Elway: Redefining Leadership and Innovation in Sports and Beyond

Lew Alcindor: Redefining Power, Identity, and Legacy in Modern Basketball

Sally Hawkins’ Husband: A Quiet Power Behind the Scene of Hollywood’s Hidden Stability