Debt-Based Crowdfunding Platforms: How Crowdfunding Is Reshaping Access to Capital

Debt-Based Crowdfunding Platforms: How Crowdfunding Is Reshaping Access to Capital

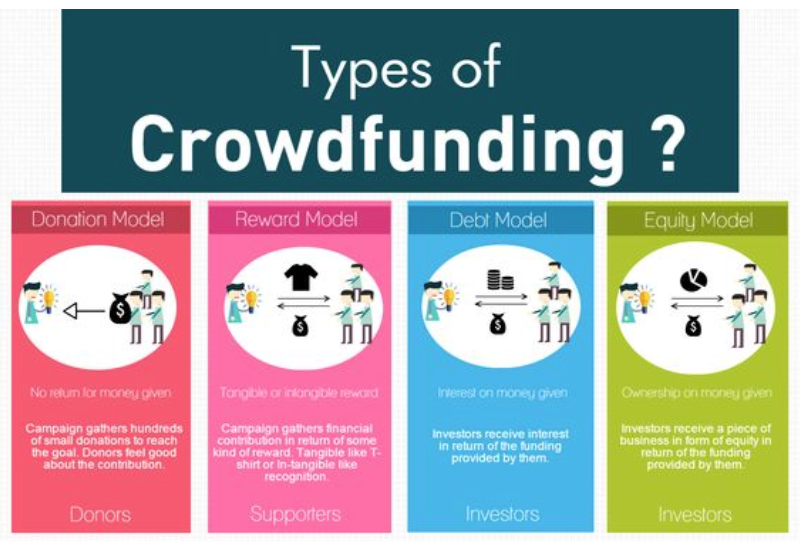

In a financial landscape shifting rapidly toward decentralized and democratized funding models, debt-based crowdfunding platforms have emerged as a transformative force—offering businesses and individuals direct access to capital without traditional gatekeepers like banks. Unlike equity crowdfunding, where investors take ownership stakes, debt-based platforms connect borrowers with a network of lenders who extend funds via peer-to-peer (P2P) or platform-mediated loans, often structured with customized repayment terms. This model empowers startups, SMEs, and even individuals to secure funding efficiently while offering investors competitive returns—all through transparent, tech-driven platforms.

As global participation in alternative finance surges, understanding the mechanics, benefits, and risks of debt crowdfunding becomes essential for entrepreneurs and investors alike.

The Mechanics of Debt-Based Crowdfunding

At its core, debt-based crowdfunding operates on a simple principle: platform users—either borrowers or lenders—join a pool of capital, with borrowers requesting loans of varying sizes and durations. These requests are then showcased based on repayment plans, creditworthiness indicators, and platform-verified risk assessments.The platform acts as an intermediary, facilitating loan agreements, managing disbursement, and overseeing repayments through automated systems or escrow mechanisms. Unlike traditional banking loans, which demand extensive collateral and credit scores, debt-based platforms often use alternative data—such as cash flow patterns, business performance metrics, and transaction histories—to evaluate creditworthiness. This democratizes access, especially for early-stage ventures and microbusinesses that may lack formal balance sheets but possess strong market potential.

Typical loan structures include fixed or variable interest rates, repayment schedules ranging from 12 to 72 months, and flexible covenants tailored to borrower profiles. Some platforms segment lenders into tiers—ranging from conservative conservators seeking low-risk returns to risk-tolerant investors willing to accept higher yields through longer tenures or unsecured loans. This segmentation allows both sides to align expectations and enhances overall platform liquidity.

Major platforms such as LendingClub, Funding Circle, and local variants in Asia and Europe exemplify how technology enables direct bonding between borrowers and a dispersed investor base. On these platforms, a simple application, backed by real-time analytics, streamlines the funding process—from origination to disbursement and repayment tracking.

Key Players and Market Evolution

Since the early 2000s, debt crowdfunding has evolved from niche P2P experiments into a major segment of fintech, growing at a compound annual rate of over 25% in key markets. The United States, United Kingdom, and China lead in scale and sophistication, but emerging economies are catching up, driven by mobile penetration and rising demand for alternative financing.Platforms like >LendingClub (US), founded in 2006, pioneered transparent, online lending by connecting individuals directly to personal and small-business borrowers, bypassing intermediaries entirely. In contrast, Funding Circle focuses primarily on small businesses, offering tailored loan packages from institutional lenders alongside community investors. In Asia, platforms such as China’s WeBank and India’s KreditBee have innovated with AI-driven credit scoring and micro-lending models that serve gig workers and informal sector enterprises.

These platforms differentiate not just in geography, but in risk profiles and regulatory compliance. For instance, European platforms frequently adhere to stringent PSD2 and ECB guidelines, ensuring investor protection and transparency, while U.S. platforms operate under SEC and state-level securities oversight.

This regulatory diversity shapes user trust and lending practices across borders.

What sets modern debt-based platforms apart is their integration of big data and AI in underwriting. Machine learning algorithms analyze thousands of behavioral and financial signals—textual data from business plans, social media activity, and even supplier relationships—to generate nuanced credit scores.

This improves loan accuracy, reduces default rates, and expands inclusive access.

Benefits for Borrowers and Lenders

For entrepreneurs and small businesses, debt-based crowdfunding offers a compelling alternative to traditional financing. The speed of capital access—often within days—contrasts sharply with weeks or months for bank loans. With streamlined applications and flexible terms, startups can secure funding precisely when needed, whether for inventory, equipment, or emergency cash flow.Beside speed, the competitive interest rates—often 2–5 percentage points lower than traditional bank offerings for similar credit profiles—reduce financing costs. Platforms also enable customizable repayment schedules, helping businesses align debt burdens with revenue cycles, a significant advantage over rigid bank amortizations. For investors, debt crowdfunding delivers tangible, predictable returns.

With transparent risk disclosures and diversified portfolios across dozens or hundreds of loans, investors mitigate concentration risk. Returns typically range from 5% to 12% annually, depending on platform benchmarks and borrower profiles, offering a middle ground between savings and riskier equity ventures. Notably, platforms often provide investor dashboards that track loan performance and default risks in real time—empowering informed decisions and adaptive portfolio management.

Startups in dynamic sectors like tech, creative industries, and green energy frequently cite faster approval and access to larger pools of capital as decisive factors in choosing debt crowdfunding over more bureaucratic routes.

Risks, Challenges, and Capital Preservation

Despite its advantages, debt-based crowdfunding carries inherent risks that demand vigilance. Borrowers face default risks that can lead to asset repossession, credit damage, or legal action—consequences amplified in unregulated or underregulated environments. Platforms vary significantly in investor protection: while U.S.and EU platforms enforce rigorous disclosure and mediation protocols, emerging-market platforms may lack equivalent safeguards, increasing exposure to fraud or platform insolvency. Lenders must also navigate heterogeneity in risk. A diversified portfolio mitigates exposure, but even well-scrutinized loans can suffer defaults during economic downturns.

Default rates, while generally lower than unsecured credit cards, historically range from 2% to 7%, varying by sector and borrower type. Transparency remains a key differentiator. High-performing platforms deliver clear, up-to-date data on loan performance, delinquency, and borrower support—enabling proactive risk management.

Investors who rely solely on platform self-reporting without independent verification face heightened risks. Furthermore, platform sustainability hinges on liquidity and operational resilience. A single major default or platform failure can erode investor confidence fast.

Regulatory oversight and capital adequacy requirements are thus critical to maintaining market stability and trust.

Successful navigation requires due diligence: scrutinizing a platform’s historical default data, liquidity buffers, and regulatory compliance, alongside diversifying across loan types and borrower segments.

Regulatory Landscape and Investor Safeguards

Globally, regulatory frameworks for debt-based crowdfunding vary, reflecting differing financial philosophies and risk appetites. In the United States, the Securities and Exchange Commission (SEC) oversees platforms under the JOBS Act and Regulation A+, mandating transparency, investor licensing, and risk disclosures.This ensures minimum safeguards—such as verified borrower profiles and clear terms—though oversight gaps persist. The European Union, through MiFID II and national securities laws, enforces stringent capital requirements and investor experience thresholds, focusing on protecting less sophisticated participants. Platforms like Lending Club’s European arm adhere to PSD2 standards, embedding data protection and anti-fraud measures directly into platform architecture.

Emerging markets often face a dual challenge: balancing innovation with consumer protection. Rapid growth outpaces regulation in regions like Southeast Asia and Africa, where mobile-based lending has exploded. Increasingly, governments collaborate with fintech groups to build regulatory sandboxes, fostering innovation while embedding consumer safeguards and dispute resolution mechanisms.

For entrepreneurs accessing debt crowdfunding, documenting loan terms, maintaining detailed repayment records, and preparing for contingencies are indispensable. Similarly, investors benefit from treating these platforms as part of a broader asset allocation strategy—complementing rather than replacing traditional markets.In sum, debt-based crowdfunding bridges a critical financing gap with speed, inclusivity, and flexibility—but success hinges on informed participation, rigorous due diligence, and ongoing risk management.

As fintech evolves, these platforms are not just alternative lenders; they are catalysts for financial democratization, empowering both givers and borrowers in an interconnected global economy.

Related Post

BDO Tax Associate: Your Strategic Pathway to a Dynamic Career in Tax and Accounting

Sarah Outer Banks: The Quiet Power Behind a Rising Creative Force on Outer Banks

Joann Fabric Careers: Where Passion for Textiles Meets Professional Growth

Revolutionary Roots: Unveiling the Life and Enduring Legacy of Joseph Simmons