Mastering the Five C’s of Credit: The Blueprint to Financial Confidence

Mastering the Five C’s of Credit: The Blueprint to Financial Confidence

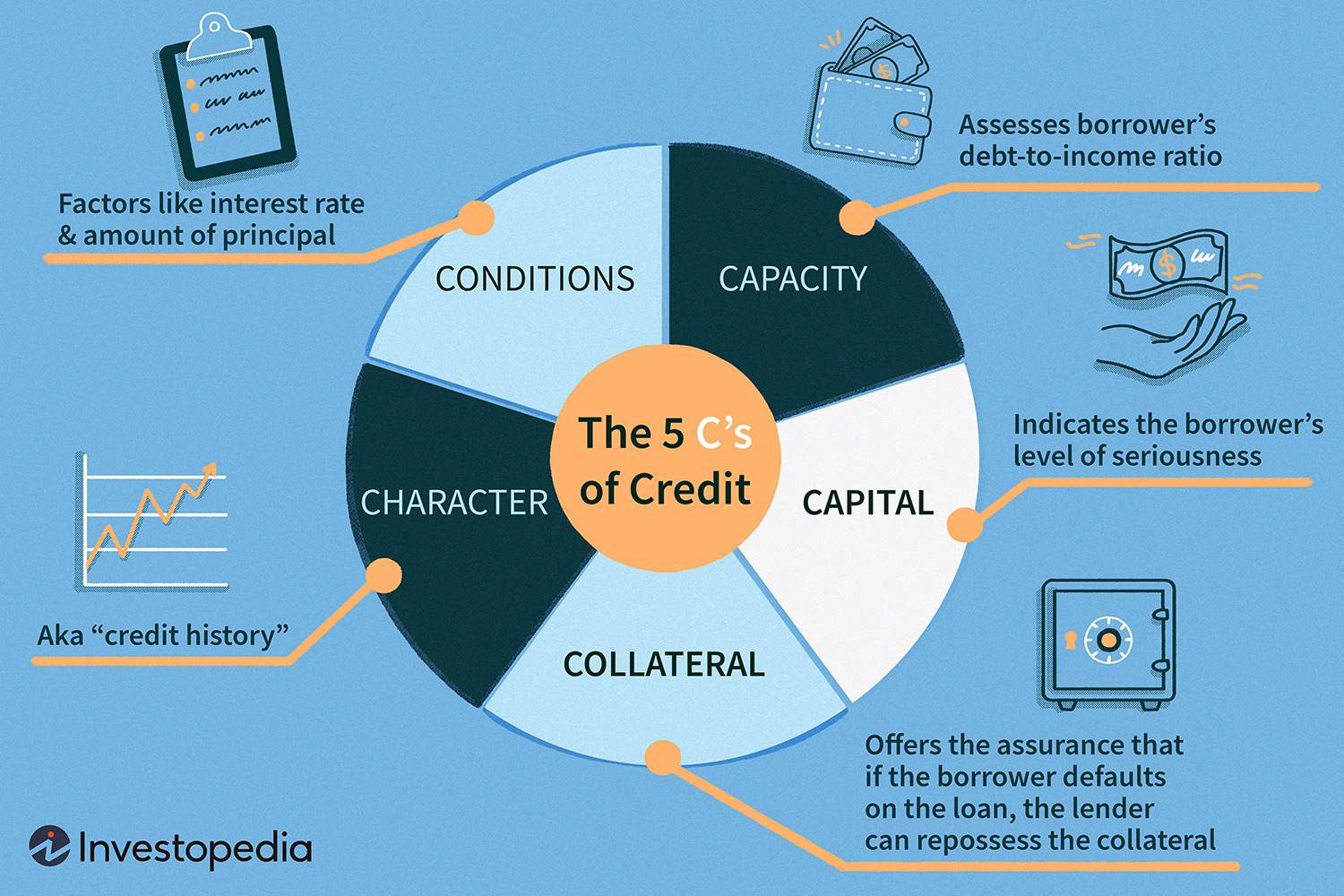

Your credit score is far more than a number — it’s a financial identity card, shaping loan approvals, interest rates, and even rental eligibility. Yet understanding how credit truly works often remains a mystery, buried under jargon and confusion. The secret lies not just in knowing what credit is, but in mastering the five core pillars that sustain and enhance it: Character, Capacity, Collateral, Credit history, and Conditions.

These five “C’s” form a comprehensive framework that guides responsible credit behavior — and empower anyone to build lasting financial strength. From defining each component in plain terms to explaining how they interrelate, this article unpacks everything you need to know to take control of your credit journey.

Character: The Foundation of Trust in Credit

At the heart of credit lies Character — the quality of trust and reliability a borrower demonstrates.Gallup research reveals that character is the most influential factor in financial decisions, accounting for up to 60% of creditworthiness in traditional scoring models. Yet difference between “good character” and “bad habits” shapes credit outcomes far more than raw data. Lenders assess integrity through payment consistency, communication honesty, and long-term responsibility.

What does strong character look like in practice? - Paying bills on time, every time — even small ones — signals dependability. - Communicating promptly when financial strain arises, rather than disappearing in crisis.

- Avoiding unnecessary debt accumulation, reflecting disciplined financial judgment. Federal Reserve studies underline that character isn’t just a vague virtue but a measurable behavior. “Consistent on-time payments over years are often more telling than perfect scores,” says Dr.

Sarah Lin, consumer finance expert at the University of Financial Studies. “Credit is a relationship, and character builds that foundation.” Taking practical steps—like setting reminders for due dates or building an emergency fund—reinforces integrity, making it easier to access favorable credit terms over time.

Capacity: Proving You Can Repay What You Borrow

Capacity measures a borrower’s ability to meet financial obligations.Unlike character, it’s quantitative: lenders analyze income, existing debt, and cash flow to determine how much you can realistically repay. The “debt-to-income” ratio — monthly debt payments divided by gross income — remains the gold standard: a ratio below 36% signals strength, while anything above 43% raises red flags. Beyond ratios, capacity includes: - Stable employment history or reliable income streams.

- Current savings that cushion monthly payments during lean months. - A realistic budget that accounts for both wants and obligations. Financial analyst Maria Cardoso emphasizes, “A high credit score without demonstrable capacity is a mirage—lenders need proof you won’t default when pressures mount.” Small, strategic choices—such as timed debt consolidation or reducing discretionary spending—can significantly improve capacity, ensuring loans remain manageable and premiums remain low.

Knowing your true capacity before borrowing protects both credit and cash flow.

Collateral: Securing Confidence with Tangible Assets

Collateral acts as insurance for lenders, reducing risk by securing a loan with a physical or financial asset. Whether it’s a home, car, or savings accounts, collateral gives banks confidence that repayment has tangible backing.Mortgages, auto loans, and secured credit cards all rely on this principle—providing protection when revenue dips. The role of collateral extends beyond actual assets: - A down payment on a home signals commitment and reduces loan exposure. - Maintaining high-value savings eases pressure if income drops mid-term.

- Pledging equity in investments can unlock larger loan amounts at competitive rates. For first-time buyers or those rebuilding credit, thrifty use of collateral-free credit—like secured credit cards—builds credibility while minimizing long-term risk. As financial strategist James Reed notes, “Collateral doesn’t guarantee forgiveness, but it preserves stability—turning credit from speculation into strategy.” When secured thoughtfully, collateral strengthens trust and expands borrowing power.

Credit History: The Timeline That Tells Your Financial Story

Credit history captures the full arc of your financial behavior over time, listing every account, payment, and closing date. Scored by agencies like Equifax, Experian, and TransUnion, this timeline shapes nearly every loan decision—from mortgage rates to cell phone contracts. Lenders cross-reference public records and private reports to gauge risk, making history a cornerstone of modern finance.Key elements of credit history include: - On-time payments boost scores by 30–40 points; late payments drop them significantly. - Length of credit history rewards long-term relationships—older, responsible accounts add value. - Mix of credit types—credit cards, auto loans, mortgages—signals balanced use.

Securing a first credit card and paying bills promptly establishes a foundation, while responsible credit utilization (ideally below 30%) keeps scores resilient. “Your credit history is like a diary of financial decisions—but only if labels are clear and entries truthful,” says credit counselor Emily Torres. Dipping into collections or maxing out cards creates irreversible red flags, so treating credit history with respect is nonnegotiable for long-term access.

Conditions: The Variable Forces That Shape Credit Access

While character, capacity, collateral, and history form a stable base, Conditions introduce the dynamic elements that influence credit decisions—from market rates to lender policies. These external variables fluctuate with economic cycles, regulatory shifts, and institutional risk assessments. Critical Condition factors include: - Economic climate: Inflation, unemployment, and interest rate shifts impact approval odds.- Lender criteria: Shop around—terms vary widely between banks and credit unions. - Risk mitigation: Tighter conditions (e.g., higher down payments) during market downturns protect lenders but challenge borrowers. - Credit policy updates: Changes in scoring models or underwriting standards redefine eligibility.

“Understanding conditions means adapting, not surrendering,” explains Robert Finch, executive at a leading credit advisory firm. “During volatile periods, applying for pre-approved lines or securing co-signer support can bridge temporary gaps.” Staying informed about market conditions empowers smarter borrowing—turning uncertainty into opportunity.

Mastering the five C’s transforms credit from an abstract number into a strategic asset.

Each pillar—character, capacity, collateral, credit history, and conditions—works in concert, shaping lender perceptions and personal financial outcomes. By building strong character through consistency, evaluating capacity honestly, securing responsibly with collateral, nurturing positive credit history, and adapting to shifting conditions, anyone can cultivate a resilient credit profile. In the evolving landscape of personal finance, these foundational elements remain the compass guiding financial freedom.

Related Post

Jack Whitehall Confirms His Sexuality: A Open, Honest Stage on Gay Identity

Wynter Pitts’ Tragic Death: Unpacking the Causes That Ignited a Public Outcry

Grumpy Disney’s Grip on Classic Tales: Ainy’s Grumble Over Flawed Happiness

How Tall Is Packgod? The Surprising Stature of the Internet’s Most Mysterious Meme Figure