Principal vs. Agent in Finance: Decoding Their Roles and Uncovering Their Critical Differences

Principal vs. Agent in Finance: Decoding Their Roles and Uncovering Their Critical Differences

In the complex ecosystem of financial markets, two roles—principal and agent—form the backbone of trust, execution, and incentive alignment, yet their responsibilities diverge sharply in practice. While both operate within contractual frameworks, the distinction lies in ownership, fiduciary duty, and financial accountability. Understanding these roles is not merely academic; it directly impacts investment outcomes, client relationships, and the integrity of financial transactions.

As markets grow more sophisticated, distinguishing between a principal—who controls capital—and an agent—who manages it on their behalf—has never been more vital. This article explores the core differences between financial principals and agents, the legal and economic implications of their roles, and how aligning their incentives shapes successful outcomes in investing and risk management.

The Fundamental Roles: Ownership and Control Explained

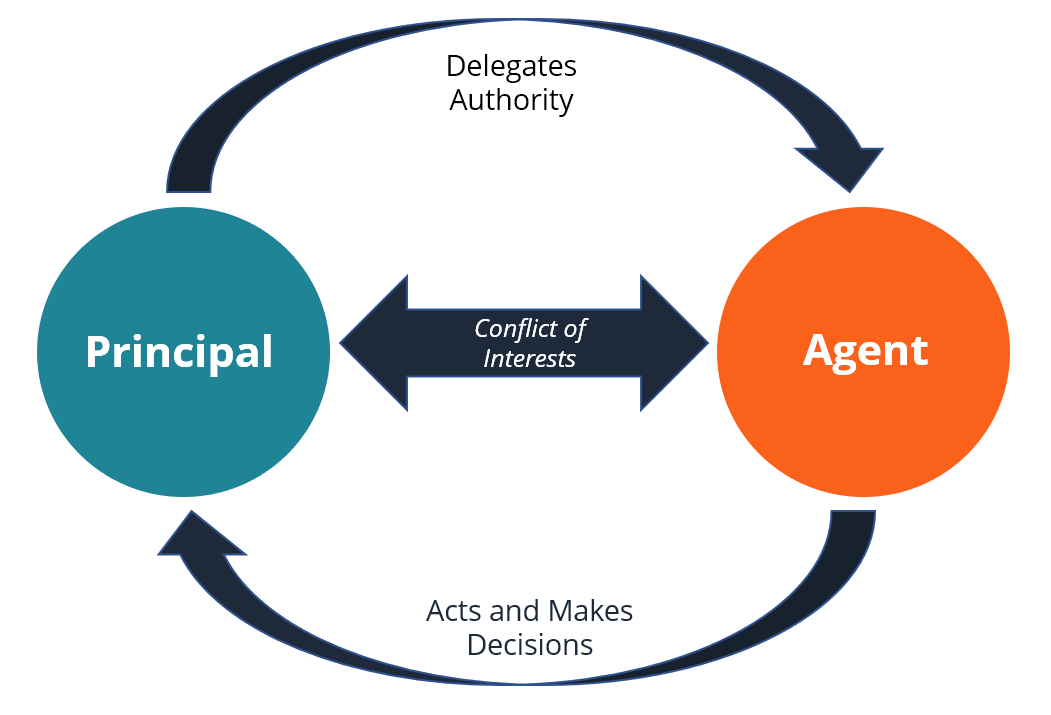

At its essence, the distinction between principal and agent centers on control and ownership.A **principal** is the entity or individual who holds legal ownership of financial assets, bearing ultimate responsibility for decision-making and bearing gains or losses. In private wealth management, for example, an individual investor who directly authorizes trades holds the principal status—owning the capital and directing strategy. Conversely, an **agent** acts as an authorized intermediary entrusted to manage, execute, or advise financial transactions.

Agents typically operate under power-of-attorney or agency agreements, wielding authority to act on behalf of the principal—but not ownership. For instance, a financial advisor managing another’s portfolio functions as an agent, making investment choices based on the principal’s instructions, but without assuming direct ownership of the assets. This dichotomy creates clear lines of authority: - **Principals** determine financial objectives, approve major strategy shifts, and accept full liability for outcomes.

- **Agents** execute actions aligned with the principal’s directives, optimize performance, but do not bear ultimate responsibility unless contractually extended. As financial writer Jonathan Merchant observes, “The principal is the owner; the agent is the executor—yet ownership defines accountability far more than authority.”

Legal Foundations: Fiduciary Duties and Conflicts of Interest

The legal framework surrounding principal-agent relationships reveals critical nuances, particularly in fiduciary obligations. A principal-agent dynamic under a fiduciary duty demands that agents prioritize their principal’s interests above their own.This standard is legally binding, creating enforceable duties of loyalty, care, and full disclosure. Firilities like bankers, portfolio managers, or insurance agents frequently operate under such obligations, legally mandated to avoid conflicts and ensure transparency. Principals retain authority under this structure—but only within defined boundaries.

Agents must operate within the scope of their authorization, and deviations may constitute breaches with legal consequences. In contrast, when a party assumes agent status without such fiduciary labeling—such as a contractor or third-party service provider—the legal recourse for mismanagement is narrower and hinges on contract enforceability rather than inherent trust. The tension between fiduciary duty and commercial models surfaces frequently in asset management.

Agents earning performance fees or charging transaction-based compensation may inadvertently prioritize profit over precise alignment with principal objectives, risking misaligned incentives—a well-documented concern in financial regulation circles.

Performance Transparency and Incentive Structures A defining difference between principals and agents lies in accountability mechanisms and incentive structures. Principals typically demand clear, measurable performance metrics—quarterly returns, risk-adjusted benchmarks, or strategic milestones—to evaluate agent effectiveness.

These metrics inform compensation, renewal terms, or penalties, ensuring agents remain accountable for outcomes. Agents, by design, do not own capital but thrive on performance-based rewards. Their incentive structures often blend fixed salaries, commissions, and bonuses tied directly to fund or portfolio returns.

For example, hedge fund managers usually earn 2% annual management fees plus 20% of profits—aligning compensation with success but also creating potential for short-termism. In contrast, a principal directly investing capital has no such performance lever, relying instead on trust, reputation, or market discipline to guide long-term value. This dynamic influences behavior: agents’ returns are scrutinized against industry standards and peer groups, while principals’ success is measured by capital preservation, capital growth, and strategic coherence—no simple ROI formulas apply.

The disparity underscores why transparency in reporting and clear KPIs are nonnegotiable when managing a principal-agent relationship.

Real-World Applications: Agents in Wealth Management and Institutional Finance

Examining practical applications clarifies how principals and agents function across financial domains. In institutional asset management, pension funds and endowments appoint investment agents—including private equity firms, hedge funds, and broker-dealers—to deploy capital on their behalf.These agents act with discretion, executing complex strategies, accessing alternative investments, and navigating market volatility. Yet, despite their autonomy, agents remain accountable through contractual service-level agreements and regulatory oversight, ensuring alpha generation remains tethered to fiduciary standards. In retail investing, platforms like Robinhood or Wealthfront represent a democratized model: users act as principals investing capital via robo-advisors functioning as agents.

The user owns assets, inputs instructions, and receives automated or human-driven portfolios. Success hinges on trust in the agent’s ability to execute efficiently and fairly—highlighting how accessible, yet delicate, these relationships have become in the age of fintech and passive investing. Even in banking, the principal-agent divide shapes product design.

Mortgage brokers (agents) serve borrowers (principals) by sourcing loans from banks (principals), balancing client interest against commission structures and lender terms. Here, transparency and conflict mitigation become paramount to avoid misaligned recommendations.

Across these varied contexts, the agent’s role is to amplify the principal’s strength—not overshadow it.

But when incentives diverge or oversight falters, the risk of mismanagement escalates, reminding stakeholders that structure defines intent—and trust depends on clarity.

Aligning Objectives: Why Misalignment Undermines Financial Success When the lines between principal and agent blur, financial outcomes suffer. Agencies compensated primarily on volume rather than long-term value may encourage excessive risk-taking or churn, eroding principal wealth. Shareholders have repeatedly penalized firms penalized by shorttermism—evident in regulatory reforms mandating better alignment through say-by-say fee disclosure or incentive clawbacks.

Conversely, when agents act as true stewards—compensated through performance tied to durable, holistic metrics—principals benefit from focused strategy investment, reduced agency costs, and enhanced returns. Universities, for instance, increasingly adopt Old-Undated structures that link endowment managers’ compensation to inflation-adjusted, long-term growth, reinforcing accountability. Studies by the Global Investment Performance Standards Council reveal that firms with strong principal-agent governance see up to 30% lower deviation from stated objectives.

Yet, enforcement remains uneven. Weak monitoring, opaque fee structures, and cognitive biases in decision-making continue to test alignment.

Ultimately, the principal-agent divide is more than a legal distinction—it’s a behavioral and economic filter shaping every financial interaction.

Those who master it build resilient portfolios; those who ignore it invite fragility.

In financial practice, recognizing whether you hold principal authority or agent responsibility determines trust, risk exposure, and strategic fidelity. As markets evolve, clarity in this fundamental relationship remains the cornerstone of sound investment stewardship—making the principal-agent dynamic not just a theoretical concept, but a practical imperative for every capital handler and custodian of value.

Understanding principal versus agent roles is not optional—it’s essential for anyone navigating the modern financial landscape. From agenda-setting to outcome accountability, these identities define who calls the shots and who carries the responsibility.

In an age where delegation is routine and trust is scarce, distinguishing these roles ensures clarity, alignment, and enduring value.

Related Post

The Rick Anthony Story: From Foster Care to a Voice for Foster Youth

Douglas Nunes Files Divorce After Years of Marriage, Citing Unresolved Tensions in Shocking Statement

Nancy Mckeon Husband: A Quiet Architect of Community Quietly Shaping American Public Life

Sean Bean’s Net Worth Revealed: From £16 Million to a Global Star with Quiet Financial Savvy